Disclaimer: Article only for educational purposes. not any But/sell recommendation.

Wonderla holidays ltd. runs the amusement parks and resorts under the flagship name of Wonderla. The company’s stock price had peaked at INR 1031 in Apr 24 and since then it has fallen to 627 currently. What has prompted a fall of 40% in share price? Have the fundamental of the company changed? or is Mr. Market gone to extremes as per his nature?

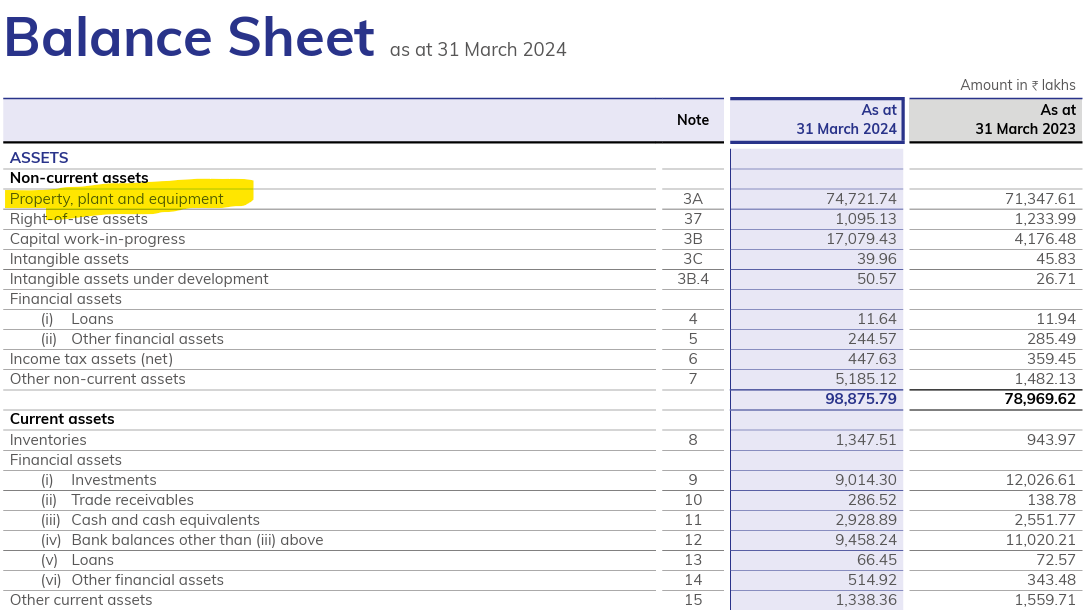

The current market capitalization of the company is approx. INR 4000 Crore while the fixed asset(INR 740 cr)combined with Investment(90 cr) and other assets(worth INR 100 Cr) in value is INR 840 crore. Which gives it a price to book multiple of INR 4 times.

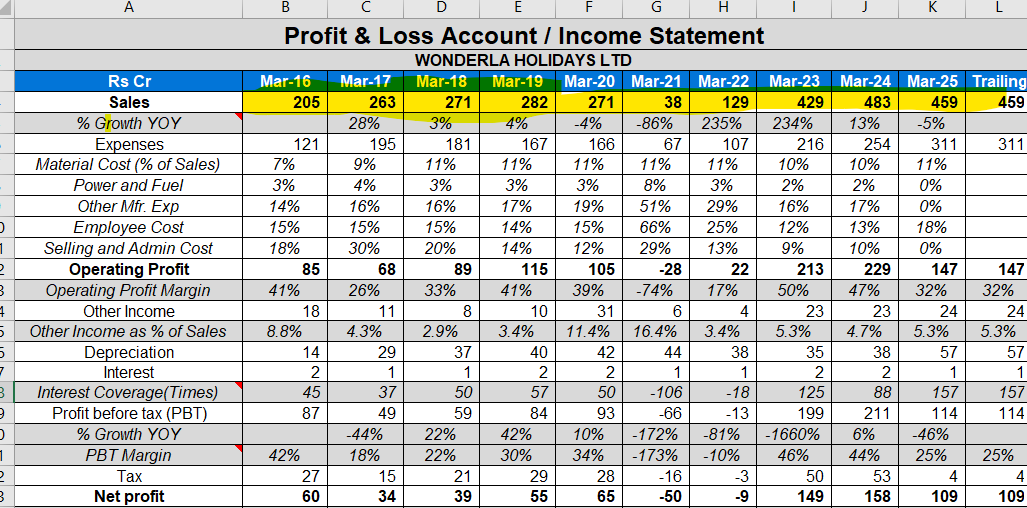

Revenue has improved from INR 129 Cr in Fy22 to 460 Cr in Fy 25 and Operating Profit has moved to 32%.

Wonderla being in amusement park business has major assets of INR 747 crores in PPE.

The company’s liquidity is strong marked with no major term debt and working capital borrowings as compared to healthy GCA of around ₹200 crore (FY24) and liquid assets balance of ₹214 crore (₹124 crore and investments in mutual funds of ₹90 crore (as on June 30, 2024: ₹224 crore)). Given that the company has negligible interest costs, owing to minimal debt profile, Wonderla has maintained PAT margins at 30-35%. The leverage and coverage metrics also remain attractive. In the past, the company has funded its capex primarily with internal accruals. Wonderla has been slowly diversifying into other states and plans to construct five new parks in the next 7-8 years. Since the company is building a new amusement park in Chennai the Capex. has zoomed from 41 Cr. in FY 23 to 170 Cr. in FY 24.

The company has an established track record of more than 20 years in the amusement park industry. While most of its competitors have not been able to successfully sustain. The company has an in-house team to modify the rides per the customers preference. Constantly invest in modifying old rides to attract footfalls. Focusing on quality and ensuring proper maintenance of rides. The company has a strong market position in south India and is now looking for expansion in the northern regions as well. It is one of the largest amusement park operators in India. The brand also has a strong recall value among the local population.

The investment thesis that we need to understand Wonderla is Capex combined with growth, availability at reasonable price. While the Capex and growth does seem to be in line , whether the company is available at reasonable price is for every investor to decide on her own.

Mr Market is on mode of correction

What a article

Keep it up !!💯💯