President Trump has bombed nuclear facilities in Iran marking the direct entry of US into Iran-Isreal conflict and threating broader economic escalations.

How is this WAR going to affect the Indian share markets? Which sectors will bear the maximum burnt and which can turn out to be possible winners? As with all things, we must look to the past to predict the future.

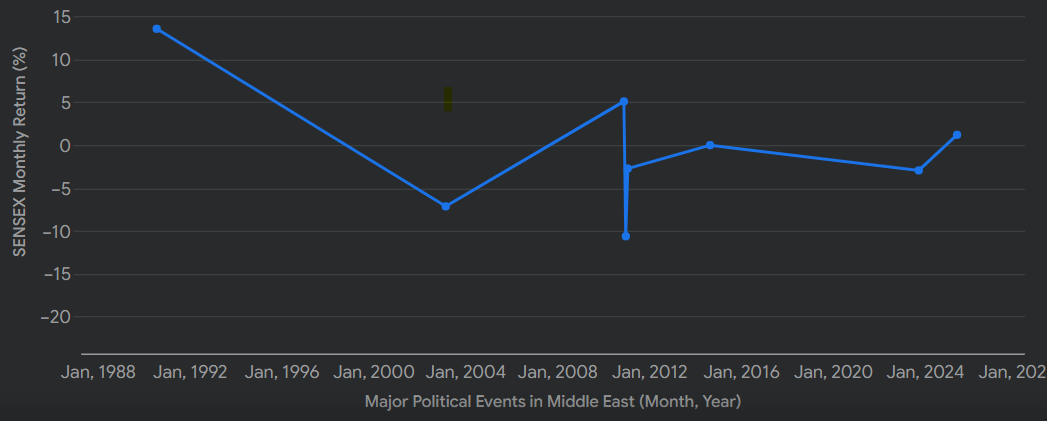

Above graph shows the SENSEX(Indian stock market benchmark Index) monthly returns during major political crisis in middles east for the past 30 years.

August, 1990 (First Gulf War start): SENSEX showed a positive return.

March, 2003 (Iraq War invasion): SENSEX experienced a negative return.

December, 2010 (Arab Spring – Tunisia): SENSEX had a positive return.

January, 2011 (Arab Spring – Egypt): This event coincided with a significant negative return for SENSEX.

February, 2011 (Syrian Civil War – Start): SENSEX showed a negative return.

September, 2014 (Yemen Civil War start): SENSEX had a positive return.

October, 2023 (Israel-Hamas Conflict): SENSEX experienced a negative return.

June, 2025 (Israel-Iran Conflict – escalation): This future event currently shows a positive return.

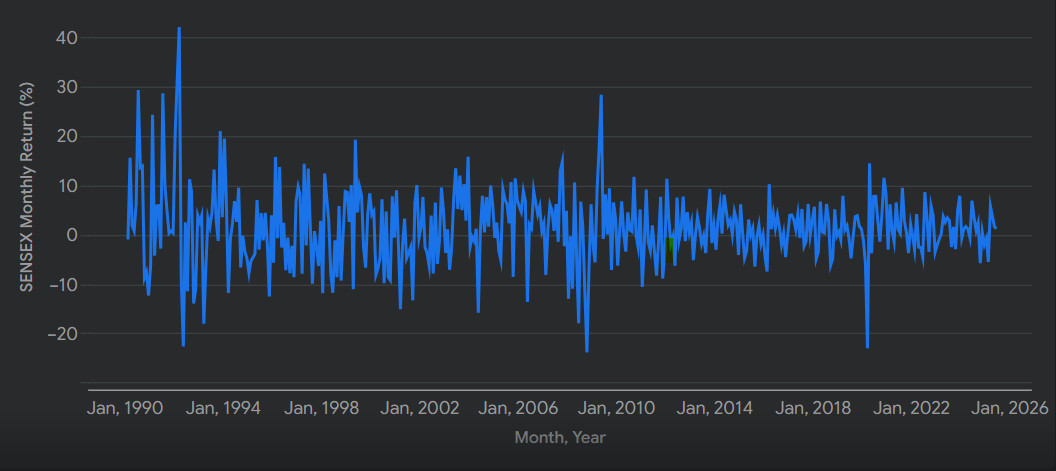

When we compare the above chart with the average monthly return of stock markets, it clearly shows that markets gyrates through a large range each month, conflict or not.

On comparing the two graphs, it becomes evident that While major Middle East political events do create headwinds but they are neither uniform nor always impacting the markets in same amount. Only the event of wider geopolitical significance like the Arab spring of Jan,2011 caused a significant decline in the markets(-10.64% in month). So the broader risk to Sensex will magnify only if the current Iran-Israel crisis takes a much bigger form.

But this situation does present an opportunity for the long-term investors to enter the equity markets or to increase the allocation to equity markets because as it is said ‘Buy when there’s blood in the streets’. An enterprising investor can find the sectors that will be most impacted by current crisis and buy the best quality businesses in this sector in this period.

Here is the list of three sectors that i feel may be impacted most and may give good entry points.

1. Petrochemicals & Chemical: No points of guessing as they are the most obvious impacted due to crude oil price surges as they rely on crude based raw materials. Paint manufactures(e.g. Asian paints ,Berger) and various chemical companies( e.g. Pidilite, SRF etc) will face higher input costs , pressurizing their profit margins.

2.Aviation and Transport: These sectors experience the double whammy of rising fuel costs and disruption to air and sea routes. Fuel cost contributes to a large portion(35-40%) of operating cost for an airline(e.g. Indigo).A surge in crude oil directly impacts the operating margins of airlines. For Shipping industries, the conflict would lead longer route(causing delay of 7-13 days), higher insurance tariffs(due to war time premiums) and supply chain disruption.

3.Certain Specific export oriented industries: Some niche export sectors could face moderate pressure, and a broader conflict could impact remittances.

a) Basmati Rice Exports: Iran is a significant market for Indian basmati rice. While it’s a staple and India has alternative markets, payment delays from conflict-hit regions could strain working capital cycles for exporters(Think KRBL).

b) Fertilizers: India has trade ties with the region for fertilizers. Disruptions could affect availability and prices of imported fertilizers, impacting the agricultural sector. Very Significant.

c) Diamonds (Cut and Polished): Israel is a trading hub for rough diamonds. While polishers have alternative hubs, a prolonged conflict could cause some disruption, though the ultimate buyers are primarily in the US and Europe.

d) Remittances: The Middle East is home to a large Indian diaspora, and remittances from this region are a major source of foreign exchange for India. A severe, prolonged conflict leading to economic instability or job losses in Gulf countries could impact these crucial remittance flows.

Please take notice that these industries’ return to normal operating condition is highly dependent on the Iran-Israel conflict remaining a regional conflict. If the conflict escalates into a larger fight, then things could be significantly worse. Since, no one has gazing ball to foresee such events, so your guess is as good as mine.