“The best time to get involved with cyclicals is when the economy is at its weakest, earnings are at their lowest, and public sentiment is at its bleakest”— Peter Lynch.

For a company long attributed as ‘LARGEST AGRO PROSSESOR OF INDIA’, Gujarat Ambuja Export ltd has been a mirage that has eluded retail investors.

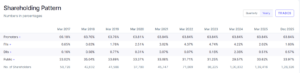

Above Shareholding pattern shows that retail investors have held almost 33% of the shares in the company for last 10 years but DII’s and FII’s have shied away from investing.

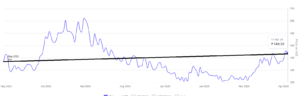

These investors have barely seen any major returns from the company in the last 3 years as the stock has barely moved 9% for the last 3 years.

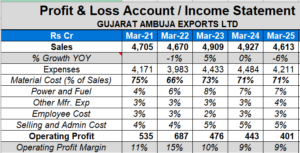

The reason, slow or minimal growth of TOP LINE, for the past 5 years the sales have barely grown but the expenses have expanded leading to low operating margins. While the topline appears to have hit a ceiling, hovering between ₹4,600 Cr and ₹4,900 Cr since 2021, this stagnation is the result of a deliberate strategic pivot rather than a lack of market demand.

To understand this pattern of sales growth, we need to understand the business of GAEL. The company has a market cap. of INR 6800 Cr. only. It procures CORN from farmers and sales the final products( Starch and other derivatives) in the market(mostly exports). That is why the RAW Material constitute almost 70% of the cost in expenses.

The company’s revenue is primarily derived from four key business segments: Maize Processing, Agro-Processing, Spinning, and Renewable Power.

Below is the breakdown of revenue from operations for the financial year (FY) 2024-25 compared to the previous year:

Segment-Wise Revenue Performance

(All figures in ₹ Crores)

| Business Segment | FY 2024-25 Revenue | FY 2023-24 Revenue |

| Maize Processing | 3,376.47 | 3,434.20 |

| Agro-Processing | 1,168.19 | 1,421.59 |

| Spinning | 60.00 | 62.40 |

| Renewable Power | 7.92* | 8.51* |

| Total Revenue from Operations | 4,612.58 | 4,926.93 |

While the maize processing business is high margin(~26%) and more value added segment, the agro-processing is low margin(~5%) and commodity type segment.

While the high margin Maize division grew at a 14% CAGR over the last 4 years, it was mathematically canceled out by the sharp revenue decline in Agro-processing (which fell 18% in FY25 alone).In FY 2021, Agro-Processing generated ₹2,578 Cr. By FY 2025, management intentionally reduced this to ₹1,168 Cr to avoid volatile commodity trading risks. In FY 2021, Agro-processing accounted for 55% of revenue. By FY 2025, its share plummeted to 25%. Simultaneously, Maize Processing revenue jumped from ₹1,958 Cr to ₹3,376 Cr.

The above pattern is a result of the deliberate and intentional attempt to make a structural shift between segments, intentionally downsizing its volatile, low-margin Agro-Processing (Soybean) segment to focus on the high-margin Maize Processing segment.

-

Timing of Capacity: Major projects, such as the 1,200 TPD Malda plant and the tripled capacity at the Hubli Maltodextrin facility, only commenced commercial production very late in the FY25 cycle. As of FY 2024-25, GAEL had roughly ₹196 Crores locked in Capital Work-in-Progress (CWIP). For an agro-processor, revenue growth is strictly limited by crushing capacity; until these plants were commissioned, sales were effectively “capped” by existing hardware limits.

- Transition From Commodity to Chemistry: On December 19, 2025, GAEL officially commenced commercial production of Sodium Gluconate. This is a high-margin specialty chemical that marks the company’s shift away from pure agro-commodity volatility.

-

NET DEBT FREE: GAEL maintains an exceptionally low Gearing Ratio of 0.07%, indicating it is virtually debt-free. With equity and reserves totaling ₹3,004 Crores against minimal borrowings of ₹217.56 Crores, the company enjoys high financial stability and lower interest sensitivity. This “deleveraged” capital structure provides the autonomy to navigate volatile commodity cycles without the pressure of fixed repayment obligations. Strategically, GAEL fuels its growth through internal accruals. It utilized its robust cash flows to fund a significant ₹281 Crore Capital Expenditure in FY 2024-25.

- Self-Sustaining Capex: In FY 2024-25, the company funded ₹281 Crores in Capital Expenditure entirely from its own cash flows. This “Debt-Free Expansion” ensures that once these assets start producing revenue, the resulting profits will belong entirely to the shareholders without being eaten by bank interest.Because the company uses internal accruals rather than debt, its Equity Base expands every year as profits are retained. However, the multi-year gestation period for mega-projects (like the ₹180 Cr Malda plant or the fermentation units) means that while the “denominator” (Equity) increases immediately, the “numerator” (Net Profit) only increases after the plants are commissioned. However, in the context of a company that is expanding capacity by 15-20% annually without taking a single rupee of term loans, this is a sign of extreme financial health.

In conclusion, GAEL has spent the last five years building a fortress. It has a deleveraged capital structure and uses internal cash to fund expansion. The data suggests the company has been “coiling” for its next jump. While the 5-year view looks flat, the Quarterly Performance for FY 2025-26 shows a massive trend reversal.

| Metric | Q1 (Jun 25) | Q2 (Sep 25) | Q3 (Dec 25) |

| Total Income | ₹1,321.59 | ₹1,505.87 | ₹1,516.54 |

| Net Profit (PAT) | ₹65.02 | ₹38.02 | ₹65.92 |

| Growth (YoY Revenue) | +21.2% | +32.0% | +33.0% |

Sales surged +31% in Q3 Dec-25 and +32% in Q2 Sep-25.This suggests that with the new capacities in Malda and Hubli finally operational and a clearer focus on ethanol and fermentation derivatives, the “stagnant” phase was merely a transition period into a more sophisticated, higher-margin business model.

The current market cap of the company is 6700 cr whereas Total Book Value (Total Shareholders’ Equity) is 3,003.96 Crores. For a debt-free company with a gearing ratio of 0.07%, a P/B of 2.26 is a strong indicator of financial health. Coming to P/E, GAEL’s P/E of ~35x might seem “expensive” at first glance. GAEL’s current valuation suggests the market is pricing it as a steady agro-processor rather than the high-margin specialty chemical player it is becoming.

Buying GAEL at this multiple is a bet on the “Specialty Chemical Transformation”—the market is finally stopping seeing it as a soybean crusher and starting to see it as a high-tech fermentation player.

But we need to remember that “markets can remain irrational longer than you can remain solvent”. So, please enter only if you have spare capital and 10 years of timeline.

Disclaimer:

ALL VIEWS ARE FOR EDUCATIONAL PURPOSES ONLY. NO BUY/SELL RECOMMENDATION.