Disclaimer: all views and opinions are personal and for educational purposes. No BUY/SELL recommendation. Take action as per your judgement.

Value lies in the eyes of the investor.

Apollo pipes Ltd.(NSE: APOLLOPIPE) is a the PVC pipes makers whose flagship company is APL apollo tubes Ltd. The company was incorporated in 2000 and the promotors have had a experience of almost 02 decades in PVC pipes industry.

APL

manufactures and markets PVC, HDPE

pipes and fittings. Further, the company’s position is supported by a strong dealership network all over

India with more than 400 distributors of which 46%

are in the north, followed by west (16%), south (19%), central (9%) and east (11%) India. Other than North India, the foray into the other regions has been recent.

APL is vulnerable to volatility in forex rates as it imports part of its raw material requirement and has negligible exports. Also, the price of resin is volatile and susceptible to changes in global prices and regional demand-supply dynamics. The company is also susceptible to cyclicality in the PVC industry. That said, the company has maintained its operating profitability, except in fiscal 2023, when profitability dipped due to steep decline in PVC resin prices.

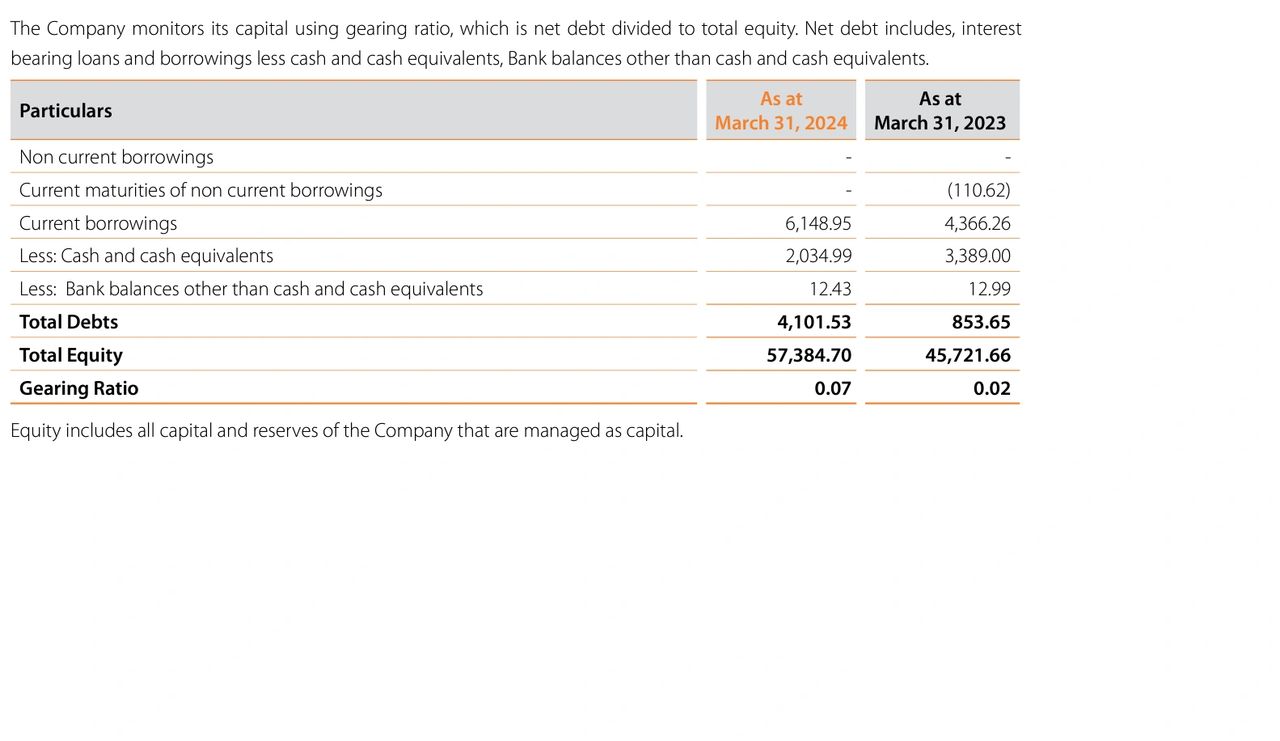

The total cash and treasury balance available with the company is only 20.34 cr. whereas the borrowings of the company are at 61.48 cr. , so the net debt for the company is 41.01 Crore, This level of debt is far from ideal for a company with total SE/net worth of 573.84 cr.

Net operating assets= Total equity + Net debt

= 573.84+41.01

= 614.85

Net profit for the year was 42.82 cr.

This gives us a operating asset return of only 7%, which is very low for any company.

Total market cap is 2098 cr for the company whereas the total sales for the company is INR 987 cr.

Year wise net debt level:

●FY 2019: (₹ 35 crore)

●FY 2020: (₹ 38 crore)

●FY 2021: (₹ 10 crore)

●FY 2022: (₹ 3 crore)

●FY 2023: ₹ 9 crore

●FY 2024: ₹ 41 crore

Apollo Pipes’ net debt saw a significant increase in FY 2024, rising from ₹ 9 crore in FY 2023 to ₹ 41 crore. This was primarily due to the company’s investment of ₹ 300 crore in capacity addition, both organic and inorganic.

Finally from the book CAPITAL RETURNS, it seems the company is working to improve the supply side of the equation. This will further lead to margin erosion.