Have you ever wondered how the phone bill and recharge amounts for keeping your contact number operation keeps rising every month. While it may pinch the consumer but for an enterprising investor this can become an opportunity in making. After undergoing multiple consolidations with the entry of Reliance Jio in 2016. The entire Indian telecom sector has become an Oligopoly of two companies, Bharti Airtel and Reliance Jio. To understand the business we must correlate with TOLL gates on a highway, once you build the highways ,one can go on collecting toll from each vehicle that crosses the road. Once a company has invested in the necessary infra upgrade and building the network requirements, the company can then go on charging the customers on subscription basis every month.

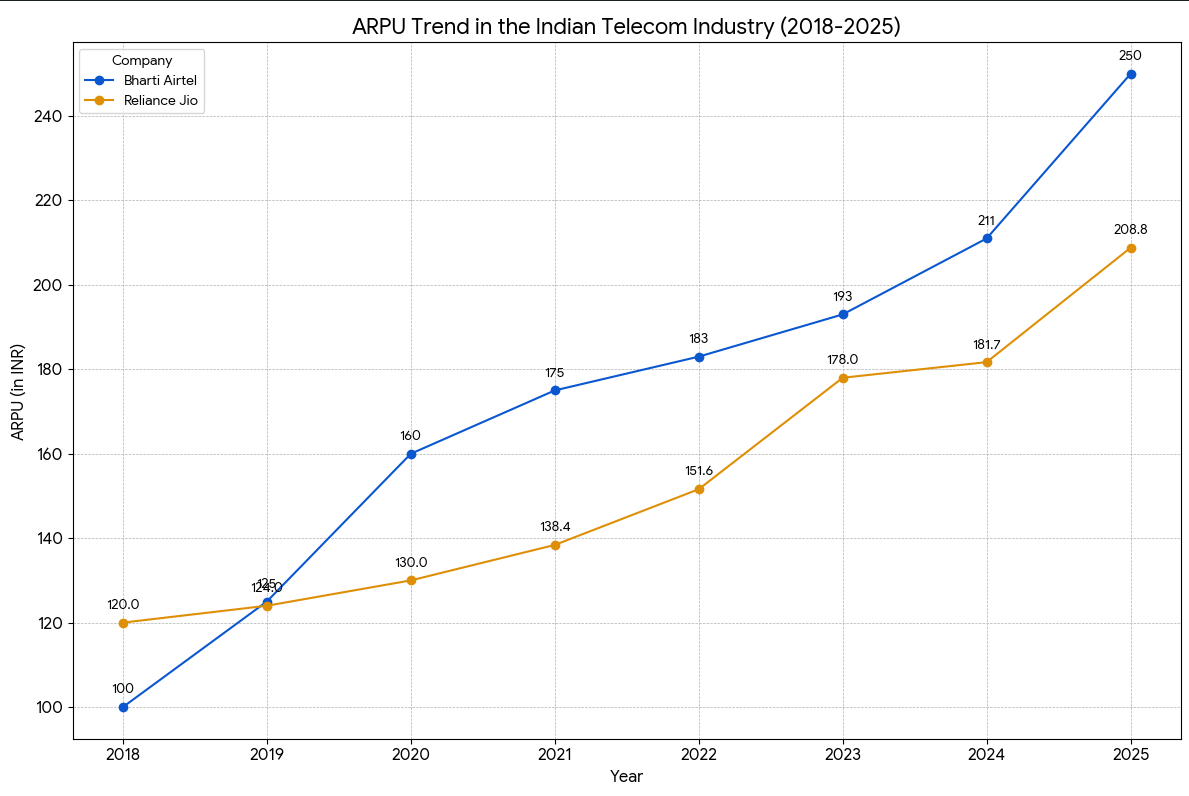

ARPU(Avg Revenue Per User) is the average amount of money a telecom operator earns from one customer. After a period of decline and intense price wars sparked by the entry of Reliance Jio, the Indian telecom sector is now witnessing a steady and significant rise in ARPU. ARPU has risen from INR 120 in 2018 to INR 250 in 2025 almost doubling in last 7 years with most of raise coming in LAST 24 months.

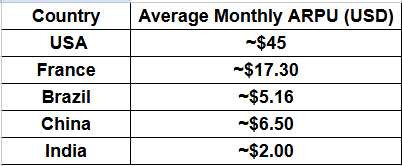

Although the ARPU’s have risen but still India has one of the lowest ARPU’s globally.This gives a long rope for the Telecome operators to keep raising the prices further.

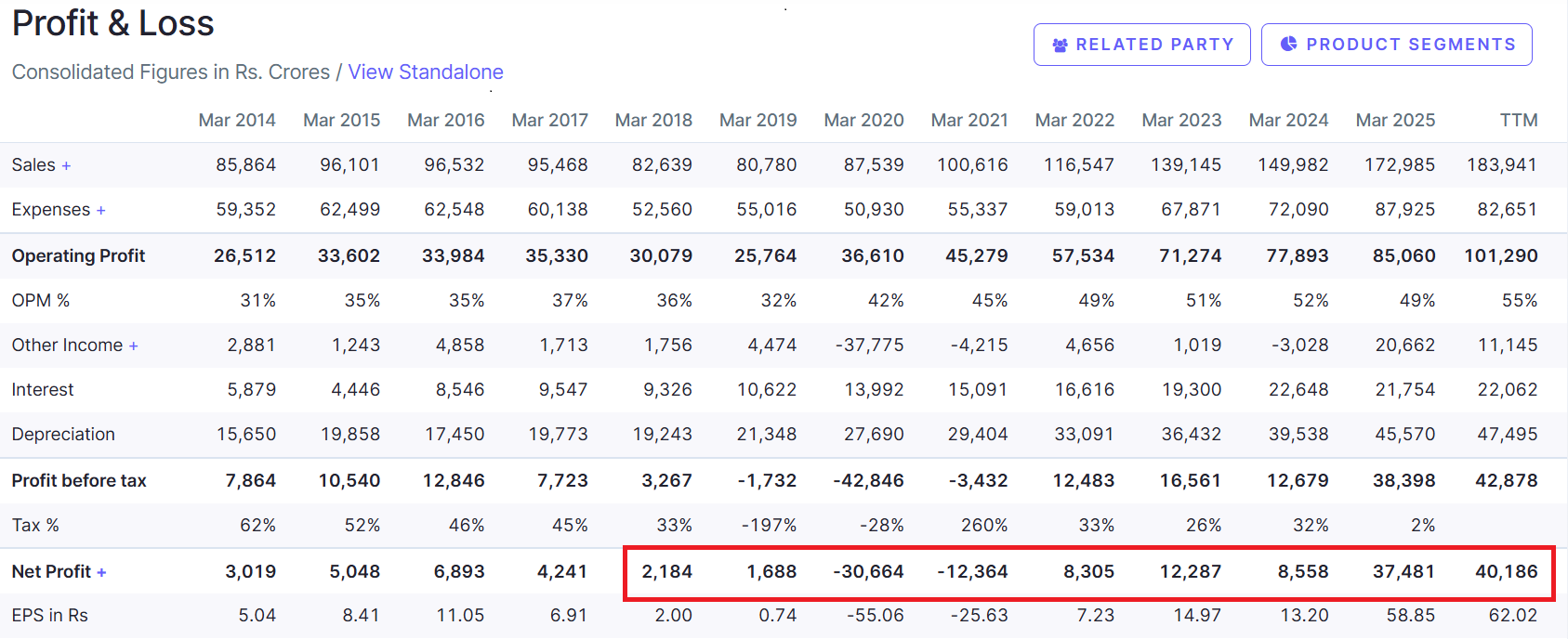

The rising ARPU has resulted in ballooning of the Revenue for the telecom operators. Below table shows the Net profit for Bharti Airtel, which has risen 10 times in the last 8 years.

The continued rise in Profit has not gone unnoticed by the market. Both FII and DII have increased shareholding in the company and stock price has zoomed to its highest mark.

Two questions that need to be answered before purchasing the stock are:

a. Will the earning’s growth continue into future at this pace? What could be the possible impediments that can come in the way?

b. The total market cap for the company is INR 11 lacs crore. Stock is trading at 10 times its book value with a PE of 39. Is it justifiable to enter the stock at this lofty valuation?

To answer the first question, it is highly likely that Bharti Airtel’s earnings will continue to rise. This is supported by several key factors observed in the Indian telecom industry and the company’s specific strategies.

Factors Driving Earnings Growth:

1. Rising ARPU: The most direct indicator of increasing earnings is the consistent and significant rise in Bharti Airtel’s Average Revenue Per User (ARPU). The company’s ARPU has been on a strong upward trajectory since 2018, climbing from a low of ₹100 to a projected ₹250 in the first quarter of FY26. This upward trend is driven by regular tariff hikes and the strategic move of discontinuing low-value plans, which forces subscribers to migrate to more expensive options.

2. Market Consolidation and Reduced Competition: The intense price wars that once decimated the industry’s profitability have largely ended. The market has consolidated into a three-player oligopoly (Bharti Airtel, Reliance Jio, and Vodafone Idea). This stability allows operators to focus on improving profitability rather than engaging in a race to the bottom, creating a more favorable environment for sustained earnings growth.

3. 5G Monetization and Subscriber Upgrades: The ongoing migration of subscribers from 4G to 5G networks is a key driver of future earnings. 5G plans are priced higher than 4G plans, directly boosting ARPU. Bharti Airtel is strategically leveraging its 5G network rollout to upsell customers and bundle premium digital services, such as streaming platforms and cloud gaming, with its high-value plans.

4. Focus on High-Value Subscribers: Airtel has a strong strategic focus on attracting and retaining high-value customers. This is evident in its higher ARPU compared to competitors and its targeted marketing of postpaid and bundled services. A high-value subscriber base provides more stable and predictable revenue streams, which contributes to overall earnings growth.

In conclusion, the combination of a disciplined market, a clear strategy to increase ARPU, and the monetization of next-generation technologies positions Bharti Airtel for continued earnings growth in the foreseeable future. The two major threats seem to be regulatory changes and major CAP EX requirement, if any arises in future.

As for the valuation front, the company does seem to be trading at high valuations with trade value being almost 10 times its book value and a PE of 39.The only way to profit for retail investors is to hold the stock for longer time frame. As the below table shows that Large caps give return only in long term.

So, in conclusion the company can provide good returns given the investor has long holding period as this is a modern TOLL business with a rising traffic and internet availability is a basic requirement for both enterprises and individuals.

DISCLAIMER: ALL VIEWS MENTIONED IN ABOVE ARTCILE ARE FOR EDUCATION PURPOSES ONLY. PLEASE DO YOUR OWN DUE DILLIGENCE BEFORE MAKING ANY DECISION.